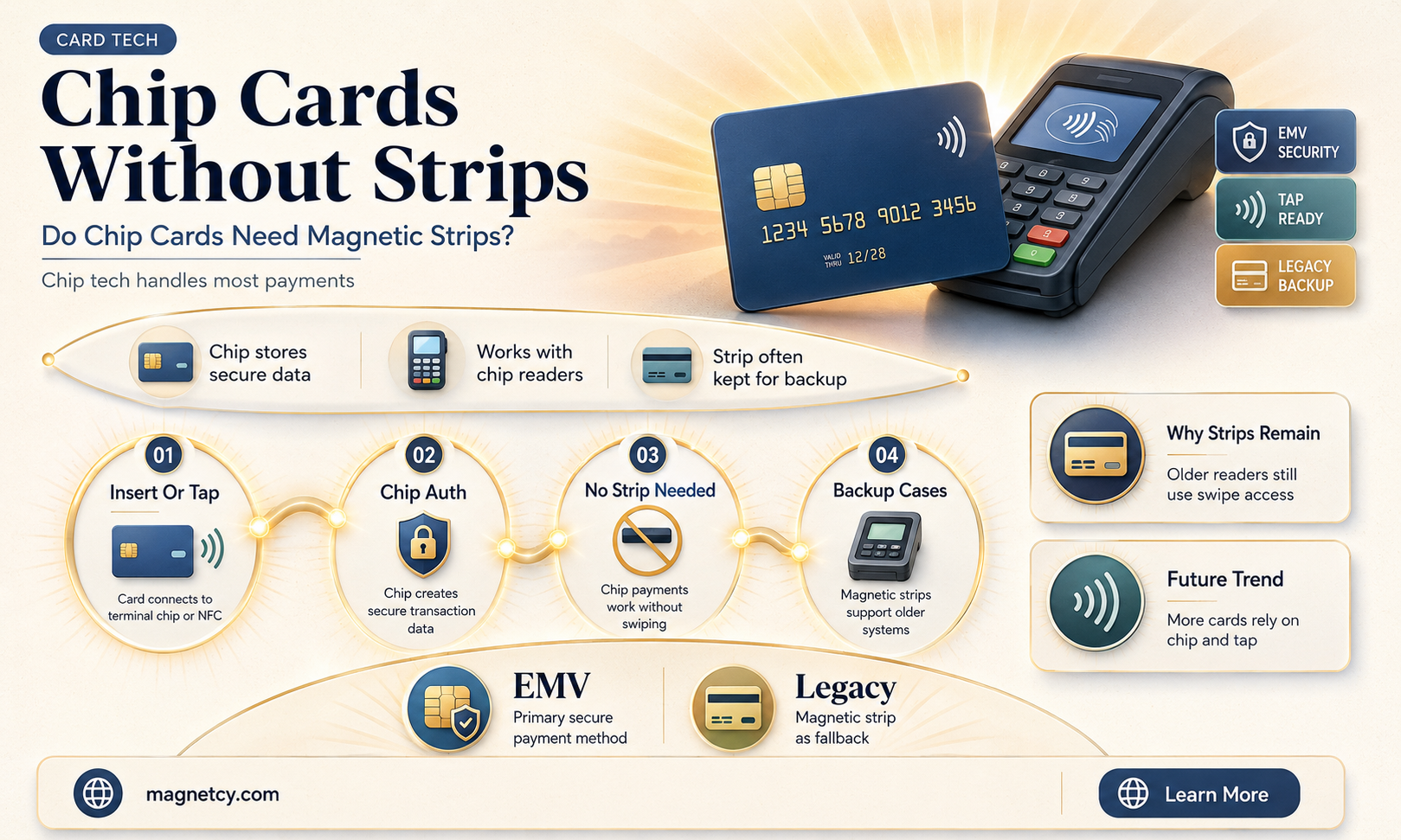

Chip cards, also known as EMV cards, are designed primarily to function using the embedded microchip for secure transactions, which has largely replaced the traditional magnetic stripe as the primary method of payment processing. While the magnetic stripe is still present on many chip cards for backward compatibility with older payment systems, the card can still work without it, as long as the merchant’s terminal supports chip technology. The chip contains encrypted data that enhances security by generating unique transaction codes, making it more difficult for fraudsters to clone or counterfeit the card. Therefore, even if the magnetic stripe is damaged or absent, the chip card remains functional at terminals equipped with chip readers, ensuring uninterrupted use for the cardholder.

| Characteristics | Values |

|---|---|

| Functionality Without Magnetic Stripe | Yes, chip cards can still work without a magnetic stripe. |

| Primary Method of Payment | EMV chip technology (inserted into a chip reader). |

| Fallback Option | Magnetic stripe can be used if chip reader is unavailable, but not required. |

| Security | Chip cards are more secure than magnetic stripe cards due to encryption. |

| Compatibility | Works with both chip-enabled and magnetic stripe-only terminals. |

| Global Adoption | Widely adopted globally, with magnetic stripes becoming less common. |

| Wear and Tear | Magnetic stripes can degrade over time; chip cards are more durable. |

| Fraud Prevention | Chips generate unique transaction codes, reducing fraud risk compared to magnetic stripes. |

| Contactless Payment | Many chip cards also support contactless payments (NFC/tap-to-pay). |

| Issuer Preference | Most issuers prioritize chip functionality over magnetic stripes. |

Explore related products

What You'll Learn

![]()

Chip vs. Magnetic Stripe Functionality

Chip cards, also known as EMV cards, have become the standard for secure transactions, but their magnetic stripes remain a fallback option. The primary function of a chip card is to generate a unique transaction code for each purchase, significantly reducing the risk of fraud compared to magnetic stripes, which store static data that can be easily cloned. If a chip card’s magnetic stripe is damaged or absent, the card can still function at terminals equipped with chip readers. However, in regions or establishments where chip technology isn’t universally adopted, a missing magnetic stripe could render the card unusable for swipe transactions.

To understand the interplay between these technologies, consider a scenario where a traveler uses a chip card abroad. In countries with advanced payment systems, the card’s chip will be the primary method of authentication, ensuring secure transactions even without a magnetic stripe. Conversely, in areas reliant on older infrastructure, the absence of a magnetic stripe could lead to declined payments. This highlights the importance of carrying backup payment methods when traveling to regions with varying levels of technological adoption.

From a security standpoint, the chip’s dynamic data encryption far surpasses the magnetic stripe’s static storage. For instance, if a magnetic stripe is skimmed, the stolen data can be used to create counterfeit cards. In contrast, the chip’s unique transaction codes are useless for fraudulent replication. This makes chip-enabled cards a safer choice, even if the magnetic stripe is compromised or missing. Consumers should prioritize using chip readers whenever possible to maximize security.

Practical tips for cardholders include verifying chip functionality before travel and ensuring the card’s magnetic stripe is intact for compatibility with older systems. If the stripe is damaged or absent, contact the issuer for a replacement card, especially before international trips. Additionally, familiarize yourself with local payment norms to avoid inconvenience. For example, in Europe, chip-and-PIN systems are prevalent, while the U.S. still relies heavily on signature verification.

In conclusion, while a chip card can function without a magnetic stripe in chip-enabled environments, its usability diminishes in areas dependent on swipe technology. Understanding the strengths and limitations of both features empowers consumers to navigate payment systems effectively, ensuring seamless transactions regardless of location or infrastructure.

Magnetic Bullet Defense: Can 20,000 Magnets Stop a Bullet?

You may want to see also

Explore related products

![]()

EMV Technology and Chip Cards

Chip cards, also known as EMV cards, have revolutionized payment security by replacing the traditional magnetic stripe with a microchip. This shift addresses the vulnerabilities of magnetic stripes, which are prone to cloning and fraud. However, a common question arises: can a chip card still function without its magnetic stripe? The answer lies in understanding the dual functionality of many EMV cards and the global adoption of EMV technology.

EMV technology, named after its developers (Europay, Mastercard, and Visa), relies on a dynamic authentication process. When inserted into a terminal, the chip generates a unique transaction code, making it nearly impossible to replicate. Unlike magnetic stripes, which store static data, the chip’s encryption ensures enhanced security. Yet, many chip cards retain a magnetic stripe as a fallback for compatibility with older payment systems, particularly in regions where EMV adoption is incomplete. This dual design allows the card to function even if the chip fails or the terminal lacks chip-reading capability.

To determine if a chip card works without the magnetic stripe, consider the transaction environment. In EMV-compliant regions like Europe and Canada, where chip readers are ubiquitous, the magnetic stripe is largely redundant. However, in areas with slower EMV adoption, such as parts of the U.S. or developing countries, the stripe remains essential. For instance, a traveler with a damaged magnetic stripe might encounter issues at a non-EMV terminal, even if the chip is intact. Practical advice: always ensure the chip is functional, but be aware of the stripe’s role in mixed-technology environments.

From a security standpoint, relying solely on the chip is ideal. The magnetic stripe’s static data makes it susceptible to skimming, a fraud method where thieves capture card information. EMV technology’s dynamic authentication significantly reduces this risk. For businesses, upgrading to EMV-compliant terminals not only enhances security but also shifts liability for fraudulent transactions back to the card issuer if the terminal is non-compliant. Consumers should prioritize using chip-enabled terminals and monitor their cards for unauthorized activity.

In conclusion, while a chip card’s primary functionality stems from its microchip, the magnetic stripe serves as a backup in non-EMV environments. As global EMV adoption continues, the reliance on magnetic stripes will diminish, but for now, their presence ensures broader usability. Understanding this duality empowers users to navigate payment systems securely and efficiently, leveraging the strengths of EMV technology while remaining prepared for legacy systems.

Are Pop Cans Magnetic? Unveiling the Truth Behind Aluminum and Magnets

You may want to see also

Explore related products

![]()

Contactless Payment Alternatives

Chip cards, also known as EMV cards, primarily rely on their embedded microchips for secure transactions, rendering the magnetic stripe largely redundant in many modern payment systems. This shift has paved the way for contactless payment alternatives, which leverage near-field communication (NFC) technology to enable faster, more secure transactions without physical contact. For instance, mobile wallets like Apple Pay, Google Pay, and Samsung Pay allow users to store their card details digitally and make payments by tapping their smartphones or smartwatches on NFC-enabled terminals. This method not only eliminates the need for a magnetic stripe but also enhances security through tokenization, where sensitive card data is replaced with unique transaction codes.

Adopting contactless payment alternatives offers several practical advantages. First, it reduces wear and tear on physical cards, as there’s no need to swipe or insert them into terminals. Second, it speeds up transaction times, with payments processing in seconds. For businesses, investing in NFC-enabled terminals is a one-time upgrade that caters to a growing consumer preference for contactless options. Individuals can maximize this technology by ensuring their devices are NFC-compatible and linking their cards to mobile wallets. A cautionary note: always enable device security features like biometric authentication or PINs to protect against unauthorized access to your digital wallet.

From a comparative perspective, contactless payment alternatives outperform traditional chip-and-stripe cards in both convenience and security. While a chip card without a magnetic stripe can still function in chip-enabled terminals, contactless methods eliminate the need for physical interaction altogether. For example, during the COVID-19 pandemic, contactless payments surged as consumers prioritized hygiene and minimal contact. This trend underscores the growing reliance on NFC technology, which is now supported by over 80% of payment terminals globally. Businesses that fail to adopt this technology risk alienating tech-savvy customers who expect seamless, touch-free payment options.

A descriptive exploration of contactless payment alternatives reveals their versatility across various contexts. In retail, self-checkout kiosks equipped with NFC readers streamline the shopping experience. In public transportation, commuters can tap their cards or devices to board trains and buses, reducing queue times. Even in informal settings like farmers’ markets, vendors use portable NFC readers to accept payments, broadening their customer base. This adaptability highlights the transformative potential of contactless technology, which is no longer a niche feature but a mainstream expectation.

In conclusion, contactless payment alternatives represent the future of transactions, offering a secure, efficient, and hygienic way to pay. By leveraging NFC technology, these methods bypass the limitations of magnetic stripes and even traditional chip cards. Whether through mobile wallets, wearable devices, or NFC-enabled terminals, the shift toward contactless payments is irreversible. For both consumers and businesses, embracing this technology is not just a convenience—it’s a strategic imperative in an increasingly cashless world.

Repetitive Transcranial Magnetic Stimulation for Seniors: 92-Year-Olds and Beyond

You may want to see also

Explore related products

![]()

Magnetic Stripe Failure Scenarios

Chip cards, also known as EMV cards, are designed to prioritize the chip for transactions, but the magnetic stripe remains a fallback option. However, magnetic stripe failure can still occur, leaving cardholders stranded if the chip is also compromised. Understanding these failure scenarios is crucial for both consumers and merchants to ensure seamless payment experiences.

Physical Damage: The most common cause of magnetic stripe failure is physical damage. Exposure to extreme temperatures, bending, or scratching can render the stripe unreadable. For instance, leaving a card in a hot car or accidentally running it through a washing machine can demagnetize the stripe. To prevent this, store cards in protective cases and avoid exposing them to harsh conditions. If damage occurs, contact your bank immediately for a replacement card.

Wear and Tear: Frequent use can lead to gradual deterioration of the magnetic stripe. Over time, the stripe's magnetic particles may become dislodged or worn down, making it difficult for card readers to retrieve data. This is particularly common in cards used for daily transactions, such as public transportation passes or loyalty cards. As a precautionary measure, periodically inspect the stripe for signs of wear and consider using contactless payment methods or the chip to extend the card's lifespan.

Interference and Corruption: External factors, such as strong magnetic fields or radio frequency interference, can corrupt the data stored on the magnetic stripe. This may occur near large electrical appliances, MRI machines, or even some types of smartphone cases with magnetic closures. While rare, data corruption can render the stripe unusable. In such cases, the chip should still function, but it's essential to monitor transaction declines and report any suspected interference to your card issuer.

Counterfeiting and Fraud: Magnetic stripe cards are more susceptible to counterfeiting and fraud due to the relative ease of duplicating stripe data. Skimming devices, for example, can capture stripe information, allowing fraudsters to create counterfeit cards. EMV chips, with their dynamic authentication process, significantly reduce this risk. However, if a fraudulent transaction occurs using the magnetic stripe, cardholders are typically protected by zero-liability policies. To minimize exposure, use chip-enabled terminals whenever possible and monitor account activity regularly.

In the event of magnetic stripe failure, the chip's presence ensures that transactions can still be completed using the more secure EMV technology. However, being aware of these failure scenarios empowers cardholders to take proactive measures, such as protecting their cards from physical damage, monitoring for wear and tear, and understanding the risks associated with magnetic stripe fraud. By doing so, they can minimize disruptions and maintain a secure payment experience.

Are Magnetic Balls Illegal in Canada? Legal Insights and Facts

You may want to see also

Explore related products

![]()

Chip Card Durability Without Magnet

Chip cards, also known as EMV cards, rely primarily on their embedded microchips for secure transactions, not the magnetic stripe. This means that even if the magnetic stripe is damaged or completely absent, the card can still function effectively at chip-enabled terminals. The chip’s durability is a key factor here—it’s designed to withstand everyday wear and tear, including exposure to heat, cold, and minor physical damage. For instance, a card dropped in water or bent slightly will often still work as long as the chip remains intact. This resilience is due to the chip’s protective casing and its ability to process data independently of the magnetic stripe.

To maximize chip card durability, consider practical steps to protect the chip itself. Avoid exposing the card to extreme temperatures, such as leaving it in a hot car or near a heater, as prolonged heat can degrade the chip’s functionality. Similarly, keep the card away from strong magnetic fields, like those found in speakers or MRI machines, which can corrupt the chip’s data. When storing the card, use a protective wallet or cardholder to shield it from physical stress, such as bending or scratching. For added safety, keep a digital record of your card details so you can quickly report it if the chip fails or the card is lost.

Comparing chip cards to their magnetic stripe-only predecessors highlights their superior durability. Magnetic stripes are prone to demagnetization, fading, and physical damage, rendering the card unusable. In contrast, the chip’s solid-state design makes it far more resistant to these issues. For example, a card with a damaged magnetic stripe might fail at a swipe terminal but work seamlessly at a chip reader. This redundancy ensures that even if one component fails, the card remains functional, reducing the likelihood of transaction disruptions.

While chip cards are robust, they’re not indestructible. Over time, repeated use can wear down the chip’s contacts, leading to connectivity issues. If you notice a card failing at chip terminals but still working with the magnetic stripe, it’s a sign the chip may be compromised. In such cases, contact your card issuer for a replacement. Additionally, be mindful of how you handle the card during transactions—inserting it forcefully or exposing it to dirt and debris can accelerate wear. Regularly inspect the chip for visible damage and clean it gently with a soft, dry cloth if necessary.

The takeaway is clear: chip cards are designed to function without relying on the magnetic stripe, thanks to the chip’s durability and independent functionality. By taking proactive measures to protect the chip, you can extend the card’s lifespan and ensure uninterrupted use. While no card is immune to damage, understanding the chip’s strengths and vulnerabilities empowers you to use it more effectively. In the rare event the chip fails, the magnetic stripe serves as a backup, though its reliability pales in comparison to the chip’s resilience. Prioritize chip-based transactions whenever possible to leverage the full benefits of this technology.

Where to Buy Earth Magnets: Top Retailers and Online Sources

You may want to see also

Frequently asked questions

Yes, a chip card can still work without the magnetic stripe, as it relies on the embedded microchip for transactions.

Magnetic stripes are included for backward compatibility with older payment terminals that don’t support chip technology.

If the magnetic stripe is damaged, the card can still function using the chip, provided the terminal supports chip transactions.

Yes, if a merchant’s terminal only accepts magnetic stripe transactions and not chip technology, the card may not work.

Yes, online purchases typically use the card number and security code, not the magnetic stripe or chip, so it will still work.